France remains one of Europe’s most structurally unique gambling markets—defined not just by its scale, but by its regulatory contrast.

Unlike fully liberalized markets such as the UK, France operates under a hybrid framework, where sports betting is regulated, while online casino remains largely unregulated. That distinction continues to shape both operator dynamics and player behavior.

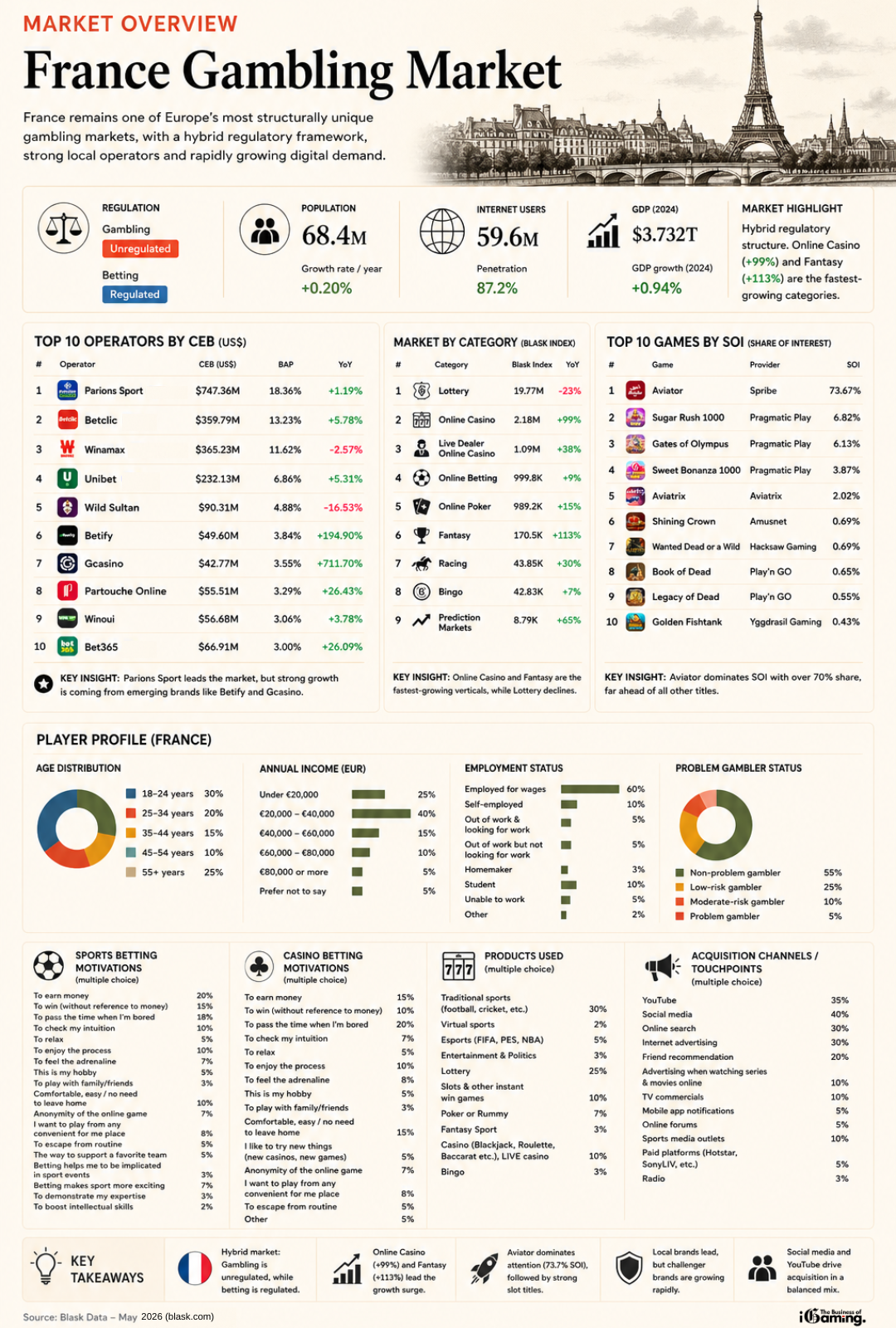

With a population of 68.4 million and nearly 60 million internet users, the country offers a sizeable, digitally active audience. But more importantly, it is a market where demand is evolving faster than regulation.

A Market Defined by Regulatory Asymmetry

France’s regulatory structure is not just a legal detail—it is the core driver of the market’s current trajectory. While sports betting operates within a clear regulatory framework, the absence of full online casino regulation has created a fragmented ecosystem. This has led to:

- Strong dominance of licensed betting operators

- Continued presence of offshore casino platforms

- Rapid growth in digital casino demand despite restrictions

At the same time, the broader economic environment remains stable, with GDP reaching $3.73 trillion in 2024 and moderate annual growth. The result is a market that is both mature and transitional—stable at the top, but shifting underneath.

Top 10 Operators by CEB (US$)

| # | Operator | CEB (US$) | BAP | YoY |

|---|---|---|---|---|

| 1 | Parions Sport | $747.36M | 18.36% | +1.19% |

| 2 | Betclic | $359.79M | 13.23% | +5.78% |

| 3 | Winamax | $365.23M | 11.62% | -2.57% |

| 4 | Unibet | $232.13M | 6.86% | +5.31% |

| 5 | Wild Sultan | $90.31M | 4.88% | -16.53% |

| 6 | Betify | $49.60M | 3.84% | +194.9% |

| 7 | Gcasino | $42.77M | 3.55% | +711.7% |

| 8 | Partouche Online | $55.51M | 3.29% | +26.43% |

| 9 | Winoui | $56.68M | 3.06% | +3.78% |

| 10 | Bet365 | $66.91M | 3.00% | +26.09% |

Key Insight

At the top, Parions Sport—backed by FDJ—continues to lead, reinforcing the strength of domestic, regulated operators. But the real story lies further down the table.

- Betify (+194.9%) and Gcasino (+711.7%) highlight explosive challenger growth

- Established brands like Winamax and Wild Sultan show mixed or declining momentum

This signals a clear shift – Growth is increasingly coming from agile, digital-first brands, rather than legacy dominance.

Read more: Online Gambling in the US

Market by Category (Blask Index)

| Category | Blask Index | YoY |

|---|---|---|

| Lottery | 19.77M | -23% |

| Online Casino | 2.18M | +99% |

| Live Dealer Online Casino | 1.09M | +38% |

| Online Betting | 999.8K | +9% |

| Online Poker | 989.2K | +15% |

| Fantasy | 170.5K | +113% |

| Racing | 43.85K | +30% |

| Bingo | 42.83K | +7% |

| Prediction Markets | 8.79K | +65% |

Key Insight

Two trends stand out clearly:

- Online Casino (+99%) and Fantasy (+113%) are driving growth

- Lottery (-23%) is declining sharply

Despite regulatory constraints, casino demand is accelerating—suggesting that player behavior is outpacing legislation.

Top Games by SOI (Share of Interest)

| # | Game | Provider | SOI |

|---|---|---|---|

| 1 | Aviator | Spribe | 73.67% |

| 2 | Sugar Rush 1000 | Pragmatic Play | 6.82% |

| 3 | Gates of Olympus | Pragmatic Play | 6.13% |

| 4 | Sweet Bonanza 1000 | Pragmatic Play | 3.87% |

| 5 | Aviatrix | Aviatrix | 2.02% |

| 6 | Shining Crown | Amusnet | 0.69% |

| 7 | Wanted Dead or Wild | Hacksaw Gaming | 0.69% |

| 8 | Book of Dead | Play’n GO | 0.65% |

| 9 | Legacy of Dead | Play’n GO | 0.55% |

| 10 | Golden Fishtank | Yggdrasil | 0.43% |

Key Insight

The dominance of Aviator (73.67%) is striking—and unlike most European markets. Crash games are not just trending in France—they are defining the market.

Meanwhile, Pragmatic Play continues to dominate the slot segment, reinforcing its position as a leading global supplier. France stands out as a market where new formats can scale extremely fast, especially in less regulated environments.

Read more: German Gambling Market

The French Player: Younger, Digital, and Diverse

The player profile reflects a relatively young and digitally engaged audience. Age distribution is balanced, with strong participation from:

- 18–24 (30%)

- 25–34 (20%)

- 35–44 (15%)

Income levels are concentrated in the mid-range, with the largest group earning between €20,000 and €40,000.

From a behavioral perspective, the majority of users fall into the non-problem gambling category (55%), though a notable share remains within low to moderate risk segments.

This suggests a market that is active and engaged, but still developing in terms of long-term behavioral patterns.

Motivations: Function Meets Entertainment

French players show a mix of motivations across verticals.

Sports betting remains driven by:

- Financial gain

- Engagement with events

- Passing time

Casino betting, meanwhile, leans slightly more toward:

- Entertainment

- Relaxation

- Curiosity around new games

The overlap between earning potential and entertainment value continues to shape product design and positioning.

Read more: Italian Gambling Market

Products and Acquisition: Digital Channels Lead

Product usage reveals a diversified ecosystem:

- Traditional sports still dominate

- Lottery remains relevant despite decline

- Slots, poker, and live casino continue to grow

On the acquisition side, the landscape is clearly digital-first:

- Social media and YouTube are key drivers

- Online search and advertising remain critical

- Organic discovery plays a smaller role compared to paid channels

👉 In a hybrid regulatory environment, visibility is often bought, not earned.

Key Takeaways

- France operates under a hybrid regulatory model, shaping market structure

- Online Casino and Fantasy are the fastest-growing verticals

- Aviator dominates game interest, highlighting crash game demand

- Challenger brands are scaling rapidly beneath established leaders

- The market is digitally driven, but structurally constrained

Read more: Brazilian Gambling Market

Final Analysis: A Market Between Two Worlds

France sits in a unique position within Europe. It has the scale and demand of a top-tier market—but not the fully liberalized structure seen elsewhere. That creates both friction and opportunity.

For operators, success in France means navigating a system where:

- Regulation defines the ceiling

- Demand pushes beyond it

- And innovation often happens in the gaps between

In that sense, France is not just another European market. It is a case study in what happens when player demand evolves faster than regulation can keep up.

{kind=link}