Brazil’s iGaming market is entering a defining phase. Long considered a high-potential but fragmented landscape, the country is now transitioning into a structured, regulated ecosystem—unlocking both scale and long-term operator opportunity.

With a population exceeding 220 million and 170 million internet users, Brazil combines sheer market size with deep digital penetration. The result is a market where demand already exists—and regulation is now accelerating its monetization.

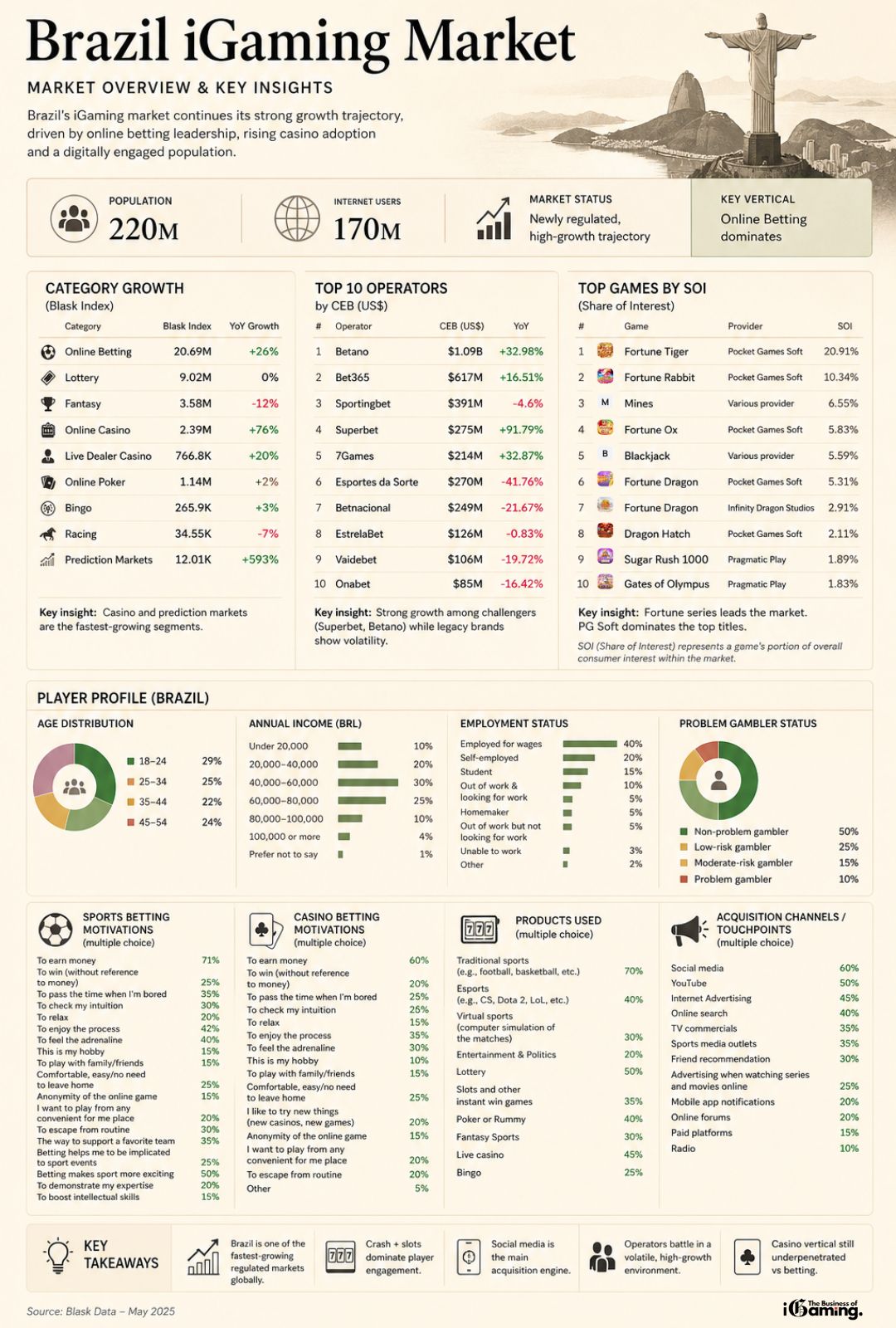

Market Overview: A Regulated Market With Immediate Momentum

| Metric | Value |

|---|---|

| Population | 220M |

| Internet Users | 170M |

| Market Status | Newly regulated |

| Key Vertical | Online Betting |

Brazil is not building demand from scratch—it is formalizing it. The regulatory shift is effectively converting an already active grey market into a structured, competitive environment. This is why growth is not gradual—it is immediate.

Online betting remains the dominant vertical for now, but early indicators suggest that the market will diversify quickly as operators push casino products more aggressively.

Category Growth: Casino Expansion Signals Market Maturity

| Category | Blask Index | YoY Growth |

|---|---|---|

| Online Betting | 20.69M | +26% |

| Lottery | 9.02M | 0% |

| Fantasy | 3.58M | -12% |

| Online Casino | 2.39M | +76% |

| Live Dealer Casino | 766.8K | +20% |

| Online Poker | 1.14M | +2% |

| Bingo | 265.9K | +3% |

| Racing | 34.55K | -7% |

| Prediction Markets | 12.01K | +593% |

The data points to a clear structural shift. While betting continues to drive volume, the fastest growth is happening elsewhere—particularly in online casino and emerging verticals like prediction markets.

This is typically what happens in newly regulated markets: betting leads early adoption, but casino drives long-term value. Brazil appears to be following that trajectory, but at a faster pace than many European markets did historically.

Read more: The UK Gambling Market

Top Operators: A Market Still Wide Open

| # | Operator | CEB (US$) | YoY |

|---|---|---|---|

| 1 | Betano | $1.09B | +32.98% |

| 2 | Bet365 | $617M | +16.51% |

| 3 | Sportingbet | $391M | -4.6% |

| 4 | Superbet | $275M | +91.79% |

| 5 | 7Games | $214M | +32.87% |

| 6 | Esportes da Sorte | $270M | -41.76% |

| 7 | Betnacional | $249M | -21.67% |

| 8 | EstrelaBet | $126M | -0.83% |

| 9 | Vaidebet | $106M | -19.72% |

| 10 | Onabet | $85M | -16.42% |

At the top, Betano and Bet365 maintain clear leadership positions, but the real story sits just below them. Challenger brands—particularly Superbet—are scaling aggressively, in some cases outpacing incumbents in growth.

At the same time, volatility among mid-tier operators highlights how competitive and unsettled the market still is. Brazil is not yet consolidated. Positioning, branding, and distribution strategies are still being tested in real time.

Top Games by SOI: Mobile-First Content Wins

| # | Game | Provider | SOI |

|---|---|---|---|

| 1 | Fortune Tiger | PG Soft | 20.91% |

| 2 | Fortune Rabbit | PG Soft | 10.34% |

| 3 | Mines | Various | 6.55% |

| 4 | Fortune Ox | PG Soft | 5.83% |

| 5 | Blackjack | Various | 5.59% |

| 6 | Fortune Dragon | PG Soft | 5.31% |

| 7 | Fortune Dragon | Infinity Dragon | 2.91% |

| 8 | Dragon Hatch | PG Soft | 2.11% |

| 9 | Sugar Rush 1000 | Pragmatic Play | 1.89% |

| 10 | Gates of Olympus | Pragmatic Play | 1.83% |

Player behavior in Brazil is strongly shaped by mobile-first design and culturally adapted content. PG Soft’s dominance—particularly through its “Fortune” series—illustrates this clearly.

Rather than traditional European slot leaders dominating outright, Brazil shows a different pattern: games that are lightweight, visually engaging, and optimized for mobile environments perform best.

This has direct implications for providers—localisation and UX matter more here than legacy brand recognition.

Player Profile: Young, Digital, and Highly Engaged

Brazil’s player base is both younger and more digitally native than many mature European markets. This shapes not only product preferences, but also how users engage with operators and content.

A large portion of players falls within the 18–34 range, and income distribution suggests strong participation from middle-income segments. Combined with high mobile usage, this creates a user base that is highly responsive to digital-first strategies.

Unlike more mature markets, where player behavior is often stable, Brazil still shows signs of rapid evolution—particularly in how users transition between betting and casino products.

Motivations: A Blend of Utility and Entertainment

There is a clear duality in player motivation. Sports betting is still largely driven by financial outcomes—earning money remains the primary driver. However, entertainment factors such as boredom, social interaction, and engagement are also significant.

Casino behavior, on the other hand, leans more toward experience. Adrenaline, enjoyment, and immersion play a larger role, which helps explain the rapid growth in slots and live casino.

This difference is critical for operators. Betting and casino cannot be marketed in the same way—they require fundamentally different engagement strategies.

Product Trends: Beyond Betting

While traditional sports betting remains dominant in usage, other verticals are quickly gaining ground.

Slots, live casino, and hybrid formats are seeing increased adoption, while lottery and poker maintain steady but less dynamic growth.

This suggests that Brazil is moving toward a more balanced product ecosystem—something typically seen in more mature markets, but happening here at an accelerated pace.

Acquisition Channels: Social Media Leads the Way

Brazil stands out as a market where social media is not just a supporting channel—it is the primary acquisition driver.

Platforms like YouTube and social networks outperform traditional search in many cases, especially when it comes to discovery and engagement.

This reinforces a broader industry trend: operators relying solely on SEO or traditional affiliate models risk missing significant portions of the audience in markets like Brazil.

Risk Profile: Growth With Responsibility

The majority of users fall into non-problem or low-risk categories, but the presence of moderate and high-risk segments highlights the importance of responsible gambling frameworks.

As regulation matures, this will likely become an increasingly important area—both from a compliance and brand perspective.

Key Takeaways

- The market combines high growth with increasing regulatory responsibility

- Brazil is transitioning from a grey market to one of the most important regulated iGaming markets globally

- Casino and emerging verticals are growing faster than traditional betting

- The operator landscape remains highly competitive and unconsolidated

- Mobile-first, localised content is driving game performance

- Social media plays a central role in user acquisition

{kind=link}