Saudi Arabia is not a regulated online gambling market. On paper, that should make it largely irrelevant to serious iGaming operators, suppliers, affiliates, and investors.

But market data tells a very different story.

Despite a strict legal framework rooted in Sharia law, offshore betting and casino brands are already competing for significant wallet share inside the Kingdom. At the same time, Saudi Arabia is aggressively positioning itself as one of the world’s most ambitious gaming and esports economies through Vision 2030, state-backed infrastructure investments, and multi-billion-dollar strategic commitments to digital entertainment.

That contradiction makes Saudi Arabia one of the most fascinating markets in global gaming today.

Officially, gambling remains prohibited. Commercially, user demand clearly exists.

For operators, the Kingdom represents both opportunity and complexity. For the wider gaming ecosystem, it may be one of the clearest examples of how consumer digital behaviour can outpace regulation.

A Market That Officially Doesn’t Exist

Saudi Arabia’s legal position on gambling is straightforward: it is prohibited. Traditional betting, casino gambling, and other forms of wagering are banned under Saudi law, with the legal framework shaped by Islamic principles that classify gambling as prohibited activity.

Yet digital markets rarely operate according to neat regulatory definitions.

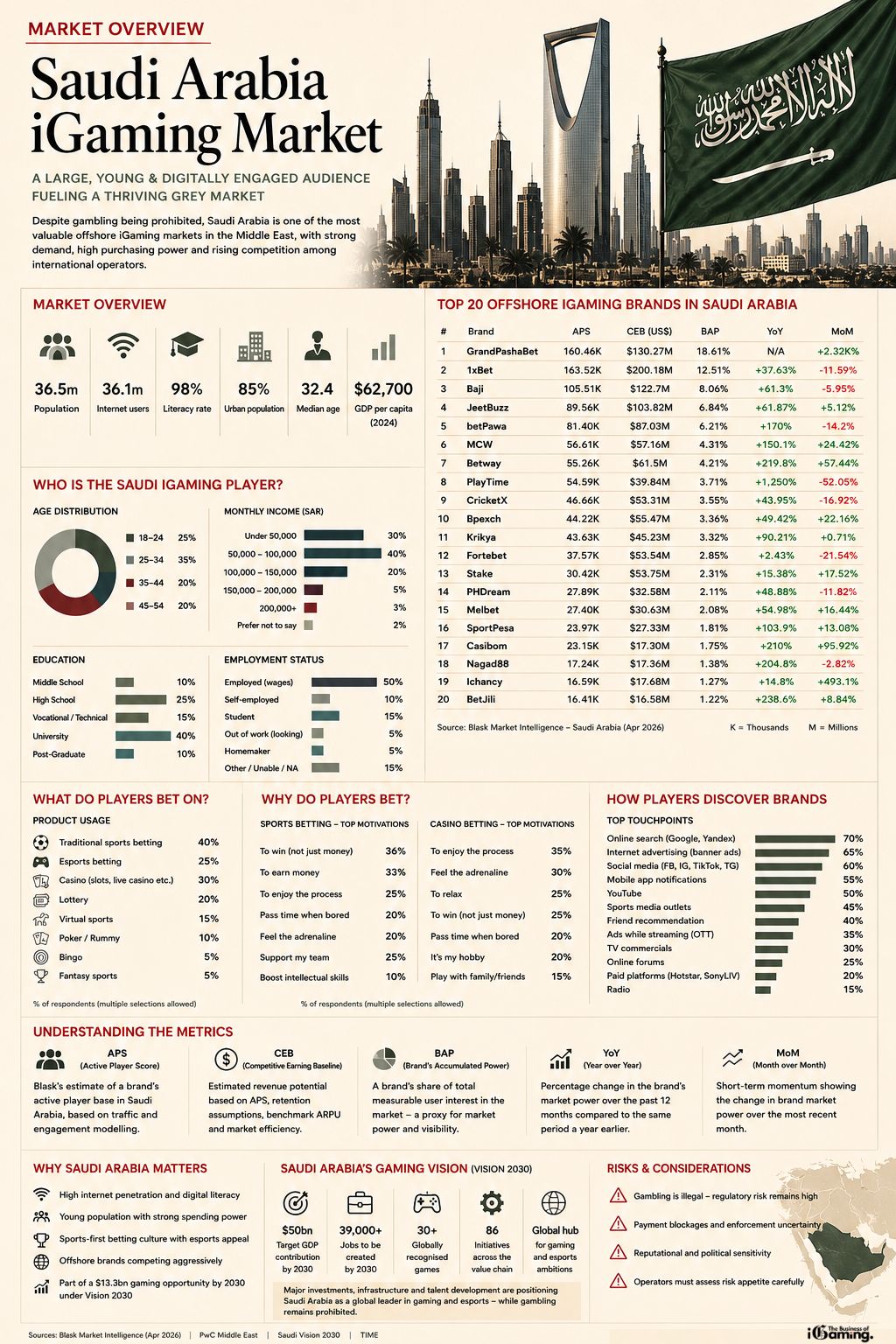

Saudi Arabia is home to approximately 36.5 million people, with internet penetration nearing universal levels at over 36 million users. Literacy stands at 98%, urbanisation is above 85%, and median age remains a youthful 32.4 years.

This matters.

Grey markets become particularly commercially attractive when they combine:

- high digital adoption

- strong purchasing power

- young mobile-first demographics

- sophisticated online consumer behaviour

- strong appetite for entertainment products

Saudi Arabia ticks every box. GDP per capita sits at roughly $62,700 according to the uploaded market profile data, placing the Kingdom far above many emerging grey-market jurisdictions where offshore operators traditionally compete.

This is not a low-value speculative market. It is a digitally mature, affluent economy where consumer demand appears to be finding unofficial routes.

Read more: The Danish Gambling Market

The Top 20 Offshore iGaming Brands Competing in Saudi Arabia

Using Blask’s Saudi Arabia market intelligence dataset, the competitive picture becomes much clearer.

Top 20 iGaming Brands by Market Presence in Saudi Arabia

| Rank | Brand | APS | CEB (US$) | BAP | YoY |

|---|---|---|---|---|---|

| 1 | GrandPashaBet | 160.46K | $130.27M | 18.61% | N/A |

| 2 | 1xBet | 163.52K | $200.18M | 12.51% | +37.63% |

| 3 | Baji | 105.51K | $122.7M | 8.06% | +61.3% |

| 4 | JeetBuzz | 89.56K | $103.82M | 6.84% | +61.87% |

| 5 | betPawa | 81.4K | $87.03M | 6.21% | +170% |

| 6 | MCW | 56.61K | $57.16M | 4.31% | +150.1% |

| 7 | Betway | 55.26K | $61.5M | 4.21% | +219.8% |

| 8 | PlayTime | 54.59K | $39.84M | 3.71% | +1,250% |

| 9 | CricketX | 46.66K | $53.31M | 3.55% | +43.95% |

| 10 | Bpexch | 44.22K | $55.47M | 3.36% | +49.42% |

| 11 | Krikya | 43.63K | $45.23M | 3.32% | +90.21% |

| 12 | Fortebet | 37.57K | $53.54M | 2.85% | +2.43% |

| 13 | Stake | 30.42K | $53.75M | 2.31% | +15.38% |

| 14 | PHDream | 27.89K | $32.58M | 2.11% | +48.88% |

| 15 | Melbet | 27.4K | $30.63M | 2.08% | +54.98% |

| 16 | SportPesa | 23.97K | $27.33M | 1.81% | +103.9% |

| 17 | Casibom | 23.15K | $17.3M | 1.75% | +210% |

| 18 | Nagad88 | 17.24K | $17.36M | 1.38% | +204.8% |

| 19 | Ichancy | 16.59K | $17.68M | 1.27% | +14.8% |

| 20 | BetJili | 16.41K | $16.58M | 1.22% | +238.6% |

Source: Blask Saudi Arabia market dataset

Understanding the Metrics

These figures are not direct operator disclosures. They are modeled competitive indicators designed to estimate relative market strength.

APS (Active Player Score)

APS represents Blask’s estimated active player footprint for a brand in the market.

This is a modeled estimate rather than exact registered account data, intended to reflect brand engagement and active market presence.

In simple terms:

Higher APS = larger estimated active player audience

CEB (Competitive Earning Baseline)

CEB estimates projected earning potential for a brand based on:

- projected APS

- user retention assumptions

- market-level average revenue per user

- modeled operational efficiency assumptions

Importantly, this is not reported gross gaming revenue.

It is a competitive estimate of what a brand could be generating under standard assumptions.

BAP (Brand’s Accumulated Power)

BAP reflects brand share of measurable user interest relative to the total competitive market index.

Think of it as a market power proxy.

Higher BAP suggests stronger overall competitive positioning.

YoY (Year-over-Year Growth)

Measures change in brand market power over the past 12 months.

Useful for identifying expansion trajectories.

MoM (Month-over-Month Momentum)

Captures shorter-term competitive momentum.

This can often reflect:

- aggressive acquisition campaigns

- promotional pushes

- sporting event seasonality

- product launches

- temporary spikes in search interest

What the Operator Landscape Tells Us

The first surprise is the absence of traditional Western dominance. Bet365 appears far down the rankings.

Stake, despite its global brand strength and strong Middle Eastern relevance, ranks outside the Saudi top ten.

Instead, the competitive landscape is fragmented and highly international. Brands with strong South Asian exposure perform particularly well:

- Baji

- JeetBuzz

- CricketX

- Bpexch

- Krikya

This suggests Saudi Arabia’s iGaming audience may not be composed solely of Saudi nationals. That would make sense.

The Kingdom hosts one of the world’s largest expatriate workforces, particularly from:

- India

- Pakistan

- Bangladesh

- Philippines

- other Asian growth markets

That changes the commercial interpretation significantly. This is not simply a domestic Saudi acquisition market. It may be a hybrid ecosystem where operators are monetising both local affluent consumers and expatriate communities.

That helps explain the prominence of cricket-centric brands.

Read more: The Swedish iGaming Market

Saudi Player Behaviour: A Commercially Attractive Audience

The customer profile data is particularly revealing.

Age Distribution

Saudi iGaming users skew young:

- 18–24: 25%

- 25–34: 35%

- 35–44: 20%

- 45–54: 20%

That means 60% of the observed audience sits under 35. This aligns closely with Saudi Arabia’s broader demographic structure. And it matters commercially. Younger cohorts tend to be:

- mobile-native

- more digitally discoverable

- more receptive to social acquisition

- more likely to engage with gamified products

- more open to esports-adjacent betting behaviour

Income & Education

Income distribution suggests meaningful spending capacity:

- 40%: SAR 50,000–100,000

- 20%: SAR 100,000–150,000

- 5%: SAR 150,000–200,000

Educational attainment is similarly notable:

- 40% university educated

- 10% post-graduate

This does not resemble a purely low-value opportunistic market. It resembles a sophisticated digital consumer base.

Read more: The Australian iGaming Market

Acquisition Channels: Where Operators Win

The touchpoint data is perhaps the most commercially useful part of the entire profile. Brand discovery sources:

- Online search: 70%

- Internet display advertising: 65%

- Social media: 60%

- Mobile app notifications: 55%

- YouTube: 50%

- Sports media: 45%

- Friend recommendations: 40%

This strongly suggests a market where performance marketing remains highly effective. Strategically:

SEO matters, paid acquisition matters, CRM matters, and influencer and social discovery matter.

That combination is catnip for performance-led operators.

Product Preference: Sportsbook Leads

Product usage data suggests sportsbook-first dynamics:

- Traditional sports betting: 40%

- Casino games: 30%

- Esports betting: 25%

- Virtual sports: 15%

- Lottery: 20%

That implies Saudi Arabia is not behaving like a slots-first LATAM or casino-heavy grey market. Instead, sports betting appears to be the primary acquisition wedge.

That changes product strategy. Winning operators likely need:

- football depth

- cricket liquidity

- live betting sophistication

- fast in-play UX

- mobile-first product design

Casino likely functions as secondary monetisation.

Read more: Gambling in Netherlands

The Vision 2030 Contradiction

This is where the story becomes genuinely interesting. Saudi Arabia is aggressively building one of the world’s most ambitious gaming ecosystems.

According to the Saudi Vision 2030 National Gaming and Esports Strategy:

- SAR 50 billion GDP contribution target

- 39,000 jobs

- 30+ globally recognised games

- 86 initiatives

- ecosystem-wide value chain development

That is extraordinary strategic ambition. The official objectives include:

- economic diversification

- digital innovation

- gaming infrastructure

- talent development

- global gaming leadership

Yet gambling remains prohibited. The distinction is deliberate. Saudi policymakers clearly separate – gaming as productive economic infrastructure from gambling as prohibited vice activity.

But commercially, the behavioural overlap is obvious. Gaming users often become betting users, and esports fans overlap with sportsbook audiences. Digital wallet familiarity increases conversion potential and gamified entertainment normalises interactive digital spending.

Read more: France Gambling Market

Saudi Arabia’s Bigger Gaming Bet

PwC’s analysis adds even more scale. The gaming and esports market is projected to generate $13.3 billion by 2030, with over $38 billion reportedly committed to sector investment.

Saudi Arabia also reportedly has 23.5 million gamers. That is astonishing market depth.

Major initiatives include:

- Esports World Cup

- gaming hubs

- developer ecosystem investments

- infrastructure projects

- technology manufacturing ambitions

This is not superficial PR spending. This is ecosystem building.

TIME’s Geopolitical Interpretation

TIME frames Saudi Arabia’s esports push as part of a broader economic transformation strategy rather than simply sports marketing.

The logic is straightforward. Saudi Arabia remains heavily exposed to hydrocarbons and diversification is essential.

Gaming offers:

- youth employment

- digital skills development

- international investment attraction

- tourism opportunities

- cultural export potential

That makes esports politically useful. It also makes digital entertainment strategically central.

Strategic Implications for Operators

If an operator chooses to target Saudi demand, what actually matters?

1. Mobile-first UX

This audience is digitally native and desktop-led experiences will underperform.

2. Arabic localisation

Still underused. Trust and conversion improve significantly with culturally relevant UX.

3. Sportsbook excellence

Football alone is not enough. Cricket clearly matters, and in-play depth matters.

4. Fast payments

Grey markets punish friction and deposit reliability becomes competitive advantage.

5. CRM sophistication

Push notifications already appear influential and retention tooling likely matters enormously.

6. Search visibility

Google remains the strongest acquisition signal and SEO remains highly strategic.

Read more: German Gambling Market

Risks and Constraints

The opportunity is real. So are the risks. Operators face:

- legal uncertainty

- payment disruptions

- enforcement unpredictability

- reputational concerns

- geopolitical sensitivity

- compliance ambiguity

Saudi Arabia is not a straightforward acquisition jurisdiction. That complexity creates both upside and risk.

Final Thoughts

Saudi Arabia may not regulate online gambling in the near future, but that does not mean the market is commercially irrelevant.

If anything, the opposite appears true. The Kingdom combines:

- affluent digital consumers

- young demographics

- strong gaming affinity

- massive esports investment

- sophisticated online behaviour

- growing offshore operator competition

That makes Saudi Arabia one of the most strategically intriguing grey markets in global iGaming. For operators, affiliates, and investors, the real question is no longer whether demand exists.

The data strongly suggests it does. The question is how long this contradiction between prohibition and participation can persist.

{kind=link}