Europe’s regulated gambling markets are often discussed in terms of scale. The UK dominates most conversations because of its size, Italy because of its regulatory significance, and Germany because of its complexity. Denmark rarely receives the same level of international attention, but that may be a mistake.

Because while Denmark is not one of Europe’s largest gambling jurisdictions by population, it is arguably one of its most structurally attractive.

This is a market defined by high digital adoption, strong consumer purchasing power, mature regulatory oversight, and player behaviour that remains heavily aligned with online casino products. It is also a market where domestic incumbents continue to perform strongly, even as international operators attempt to gain share.

The latest market data suggests Denmark remains one of Europe’s most stable and sophisticated iGaming environments—but beneath that maturity, there are still notable shifts taking place. International challenger brands are growing, casino remains overwhelmingly dominant, and certain emerging segments are showing early signs of acceleration.

For operators, suppliers, affiliates, and investors, Denmark remains a market worth watching.

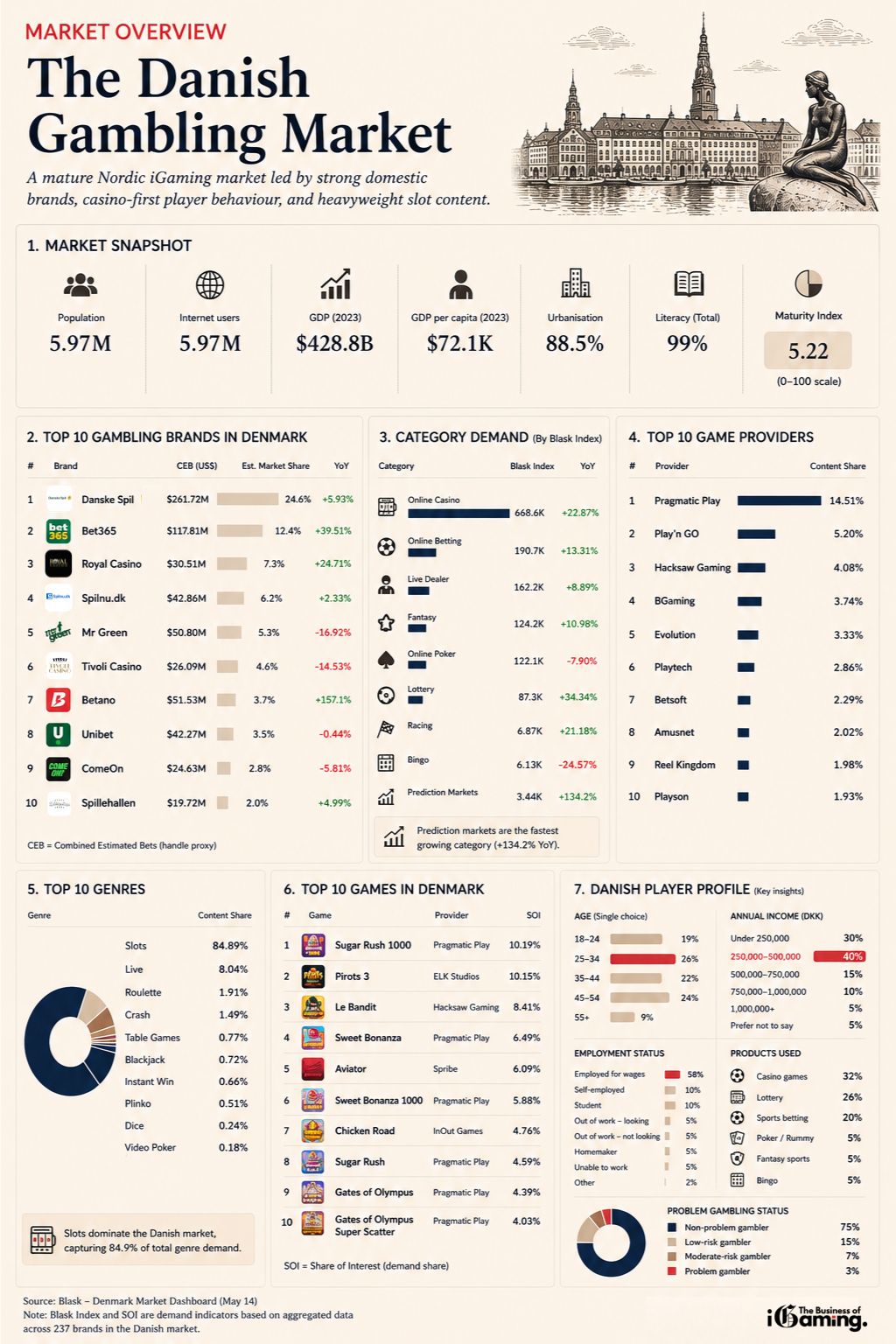

Denmark at a glance

Before diving into operator competition and player behaviour, it helps to understand the broader economic and digital context that underpins the Danish market.

| Metric | Value |

|---|---|

| Population | 5.97 million |

| Internet users | 5.97 million |

| GDP (2023) | $428.8 billion |

| GDP per capita | $72,100 |

| Urbanisation | 88.5% |

| Literacy | 99% |

| Maturity Index | 5.22 |

Few regulated markets in Europe combine such strong digital infrastructure with this level of consumer affluence.

With internet penetration effectively universal and GDP per capita among the highest in Europe, Denmark offers exactly the kind of environment operators favour: digitally fluent consumers with disposable income and strong familiarity with online services.

This helps explain why Denmark has developed into such a robust regulated gambling ecosystem despite its relatively modest population size.

What Denmark’s maturity score actually means

The Danish market’s maturity index currently stands at 5.22.

Blask defines this as a ratio-based indicator comparing combined category-level demand against aggregate brand demand. In simple terms, higher scores suggest that consumer interest in gambling categories exceeds specific brand attachment, creating a more competitive environment with broader market awareness.

That matters.

In less mature markets, brand familiarity often remains narrow. Players gravitate toward a small number of familiar operators, making it difficult for challengers to break through.

In Denmark, the opposite dynamic appears to be in play.

Consumers clearly understand the product categories themselves – casino, betting, lottery, live dealer -which means competition becomes less about introducing players to online gambling and more about winning them from competitors.

That creates a tougher operating environment, but also a healthier one.

Read more: The Australian Gambling market

Denmark’s operator hierarchy remains domestic – but challengers are moving

Despite the internationalisation of European gambling, Denmark’s operator leaderboard still shows the importance of local trust and legacy positioning.

Top 10 gambling brands in Denmark

| Rank | Brand | CEB (US$) | Estimated Market Share | YoY |

|---|---|---|---|---|

| 1 | Danske Spil | $261.72M | 24.6% | +5.93% |

| 2 | Bet365 | $117.81M | 12.42% | +39.51% |

| 3 | Royal Casino | $30.51M | 7.34% | +24.71% |

| 4 | Spilnu.dk | $42.86M | 6.2% | +2.33% |

| 5 | Mr Green | $50.80M | 5.31% | -16.92% |

| 6 | Tivoli Casino | $26.09M | 4.58% | -14.53% |

| 7 | Betano | $51.53M | 3.68% | +157.1% |

| 8 | Unibet | $42.27M | 3.49% | -0.44% |

| 9 | ComeOn | $24.63M | 2.78% | -5.81% |

| 10 | Spillehallen | $19.72M | 1.98% | +4.99% |

Danske Spil’s continued leadership is hardly surprising. As Denmark’s state-backed gambling operator, it benefits from longstanding consumer trust, extensive recognition, and a historical position that many international competitors simply cannot replicate.

A near 25% estimated share in a mature competitive market is significant.

But perhaps the more interesting story is not the incumbent leader—it is the challengers behind it. Bet365’s nearly 40% year-on-year growth is notable.

The operator has long proven its ability to scale internationally, but Denmark appears to be offering particularly strong traction. This suggests that while domestic trust remains important, global operators with strong product execution and marketing sophistication can still capture meaningful share.

Then there is Betano. A staggering 157.1% YoY growth immediately stands out.

Even if this comes from a smaller base, this is the type of movement that deserves attention. Kaizen Gaming’s expansion strategy across regulated markets has already reshaped competitive landscapes elsewhere, and Denmark may increasingly become another example.

Not everyone is moving in the same direction.

Mr Green, Tivoli Casino, and ComeOn all show contraction, suggesting mature markets do not guarantee defensive stability.

Read more: The Swedish gambling market

Denmark is overwhelmingly a casino market

If operator competition tells one story, category demand tells another. And that story is very clear.

Denmark is not primarily a sportsbook market. It is a casino-first gambling economy.

Category demand in Denmark

| Category | Blask Index | YoY |

|---|---|---|

| Online Casino | 668.6K | +22.87% |

| Online Betting | 190.7K | +13.31% |

| Live Dealer Online Casino | 162.2K | +8.89% |

| Fantasy | 124.2K | +10.98% |

| Online Poker | 122.1K | -7.9% |

| Lottery | 87.27K | +34.34% |

| Racing | 6.87K | +21.18% |

| Bingo | 6.13K | -24.57% |

| Prediction Markets | 3.44K | +134.2% |

Online casino demand dwarfs everything else. At 668.6K, it exceeds online betting by a wide margin and remains the defining commercial engine of the market.

That has major implications. For operators, casino-first markets behave differently:

- acquisition economics often revolve around casino conversion

- retention strategies are content-led

- provider relationships become more strategically important

- bonus mechanics behave differently than sportsbook-led markets

Live dealer also remains remarkably strong. This reinforces the idea that Danish players are not merely casual slot users—they are comfortable with deeper digital gambling engagement.

Poker’s decline aligns with broader international trends, while bingo’s sharp contraction suggests continued structural weakness in traditional digital social gambling formats.

Prediction markets deserve a separate mention. Yes, the base remains tiny. But triple-digit growth often signals emerging consumer experimentation worth tracking.

Read more: Gambling Market in the Netherlands

Provider dominance tells a familiar story

Casino-led markets are ultimately shaped by content. And in Denmark, one provider remains well ahead of the field.

Top 10 game providers in Denmark

| Rank | Provider | Content Share |

|---|---|---|

| 1 | Pragmatic Play | 14.51% |

| 2 | Play’n GO | 5.2% |

| 3 | Hacksaw Gaming | 4.08% |

| 4 | BGaming | 3.74% |

| 5 | Evolution | 3.33% |

| 6 | Playtech | 2.86% |

| 7 | Betsoft | 2.29% |

| 8 | Amusnet | 2.02% |

| 9 | Reel Kingdom | 1.98% |

| 10 | Playson | 1.93% |

Pragmatic Play’s lead is substantial. A 14.51% content share places it well ahead of every other supplier.

That is not merely a reflection of content quantity. It is a sign of operator integration success, commercial leverage, and product-market fit.

Pragmatic has increasingly become the default commercial slot engine across many regulated markets, and Denmark appears no different.

Play’n GO’s position makes sense in a Nordic context. The supplier remains particularly strong in European regulated ecosystems where established operator relationships and recognisable slot portfolios still matter.

Hacksaw’s presence also stands out. The company’s rapid expansion across regulated markets has been difficult to ignore, and Denmark’s appetite for high-volatility, modern slot content appears aligned with its product style.

Evolution’s ranking may seem lower than expected, but that reflects Denmark’s broader slot-heavy consumption rather than weakness in live casino.

Read more: The UK Gambling market

Danish players overwhelmingly prefer slots

The genre breakdown leaves little room for ambiguity.

Top genres in Denmark

| Genre | Share |

|---|---|

| Slots | 84.89% |

| Live | 8.04% |

| Roulette | 1.91% |

| Crash | 1.49% |

| Table Games | 0.77% |

| Blackjack | 0.72% |

| Instant Win | 0.66% |

| Plinko | 0.51% |

| Dice | 0.24% |

| Video Poker | 0.18% |

Nearly 85% of genre demand belongs to slots. That is extraordinary concentration.

This tells us Denmark is not simply casino-friendly—it is deeply slot-centric.

Live casino’s 8% share is respectable, but nowhere near enough to challenge slots’ dominance.

Crash gaming is gaining visibility, driven by titles like Aviator and Chicken Road, but remains niche relative to classic slot content.

For suppliers, the message is straightforward: Denmark rewards slot distribution.

Read more: iGaming Market in Italy

The actual games Danish players care about

Provider market share is useful. But individual title performance reveals where consumer attention actually sits.

Top 10 games in Denmark

| Rank | Game | Provider | SOI |

|---|---|---|---|

| 1 | Sugar Rush 1000 | Pragmatic Play | 10.19% |

| 2 | Pirots 3 | ELK Studios | 10.15% |

| 3 | Le Bandit | Hacksaw Gaming | 8.41% |

| 4 | Sweet Bonanza | Pragmatic Play | 6.49% |

| 5 | Aviator | Spribe | 6.09% |

| 6 | Sweet Bonanza 1000 | Pragmatic Play | 5.88% |

| 7 | Chicken Road | InOut Games | 4.76% |

| 8 | Sugar Rush | Pragmatic Play | 4.59% |

| 9 | Gates of Olympus | Pragmatic Play | 4.39% |

| 10 | Gates of Olympus Super Scatter | Pragmatic Play | 4.03% |

Pragmatic Play dominates. Again.

Its titles occupy half of the top ten, with multiple franchise extensions performing strongly. This reflects a broader industry reality.

Top-performing slots increasingly behave like entertainment IP. Sugar Rush and Gates of Olympus are no longer merely games—they are brands.

Pirots 3’s performance is particularly interesting. ELK Studios has historically resonated well with Nordic audiences, and this suggests regional relevance still matters despite the internationalisation of supplier competition.

Crash games breaking into the top ten also reinforces gradual behavioural diversification.

Read more: The German Gambling Market

Who are Denmark’s online gambling players?

Raw market demand is one thing. Understanding the people behind it is another. Blask’s customer profile data offers a useful snapshot.

Age distribution

| Age Group | Share |

|---|---|

| 18–24 | 19% |

| 25–34 | 26% |

| 35–44 | 22% |

| 45–54 | 24% |

| 55+ | 9% |

This is not purely a Gen Z market. The strongest segments are mature working-age consumers.

That matters because older demographics typically display higher spending consistency and stronger retention behaviour.

Income profile

| Annual Income (DKK) | Share |

|---|---|

| Under 250,000 | 30% |

| 250,000–500,000 | 40% |

| 500,000–750,000 | 15% |

| 750,000–1,000,000 | 10% |

| 1,000,000+ | 5% |

This reflects a commercially attractive audience. Middle-income working consumers dominate.

Combined with Denmark’s strong purchasing power, that supports sustainable monetisation.

Read more: The iGaming Market in France

Employment status

| Employment Status | Share |

|---|---|

| Employed | 58% |

| Self-employed | 10% |

| Student | 10% |

| Out of work (looking) | 5% |

| Out of work (not looking) | 5% |

| Homemaker | 5% |

| Unable to work | 5% |

| Other | 2% |

Again, this points toward economically active mainstream consumers—not fringe participation.

What products Danes actually use

Gambling product usage

| Product | Share |

|---|---|

| Casino Games | 32% |

| Lottery | 26% |

| Sports Betting | 20% |

| Esports | 15% |

| Slots / Instant Win | 10% |

| Poker / Rummy | 5% |

| Fantasy Sports | 5% |

| Bingo | 5% |

Casino’s leadership remains obvious. Lottery’s strength also reinforces Denmark’s continued hybrid gambling behaviour, where legacy formats remain commercially relevant.

Brand discovery is increasingly digital-first

Brand touchpoints

| Channel | Share |

|---|---|

| Social media | 40% |

| YouTube | 35% |

| Online search | 30% |

| Internet advertising | 25% |

| Friend recommendations | 20% |

| TV commercials | 15% |

This matters for operators and affiliates alike. Traditional advertising still has relevance. But digital discovery clearly dominates.

Search, social, and video remain central battlegrounds.

Read more: Online Gambling in Brazil

Responsible gambling indicators remain comparatively stable

Gambling risk segmentation

| Category | Share |

|---|---|

| Non-problem gambler | 75% |

| Low-risk gambler | 15% |

| Moderate-risk gambler | 7% |

| Problem gambler | 3% |

This aligns with expectations for mature regulated markets. It does not eliminate regulatory scrutiny, but it suggests relatively stable player behaviour compared with more volatile or less regulated ecosystems.

Strategic conclusions

Denmark may not dominate European gambling headlines, but it remains one of the continent’s most commercially sophisticated regulated markets.

Several conclusions stand out. First, this remains a casino-led economy. Operators entering Denmark with sportsbook-first assumptions may misread the opportunity.

Second, slots remain the commercial backbone of the ecosystem. Provider positioning, game distribution, and branded slot performance matter enormously.

Third, domestic trust still matters—but international challengers can absolutely scale. Bet365 and Betano prove that.

Fourth, mature does not mean stagnant. Growth remains visible across multiple segments.

And finally, Denmark’s combination of regulation, consumer purchasing power, and digital maturity makes it one of Europe’s most structurally attractive medium-sized gambling markets.

For suppliers, operators, affiliates, and investors alike, that makes Denmark far more important than its population alone would suggest.

{kind=link}