Germany’s gambling market doesn’t move in headlines — it moves in structure.

As one of Europe’s most tightly regulated environments, the country has built a market defined less by volatility and more by discipline. That makes it, in many ways, a benchmark for what a mature iGaming ecosystem looks like: large, stable, and increasingly competitive beneath the surface.

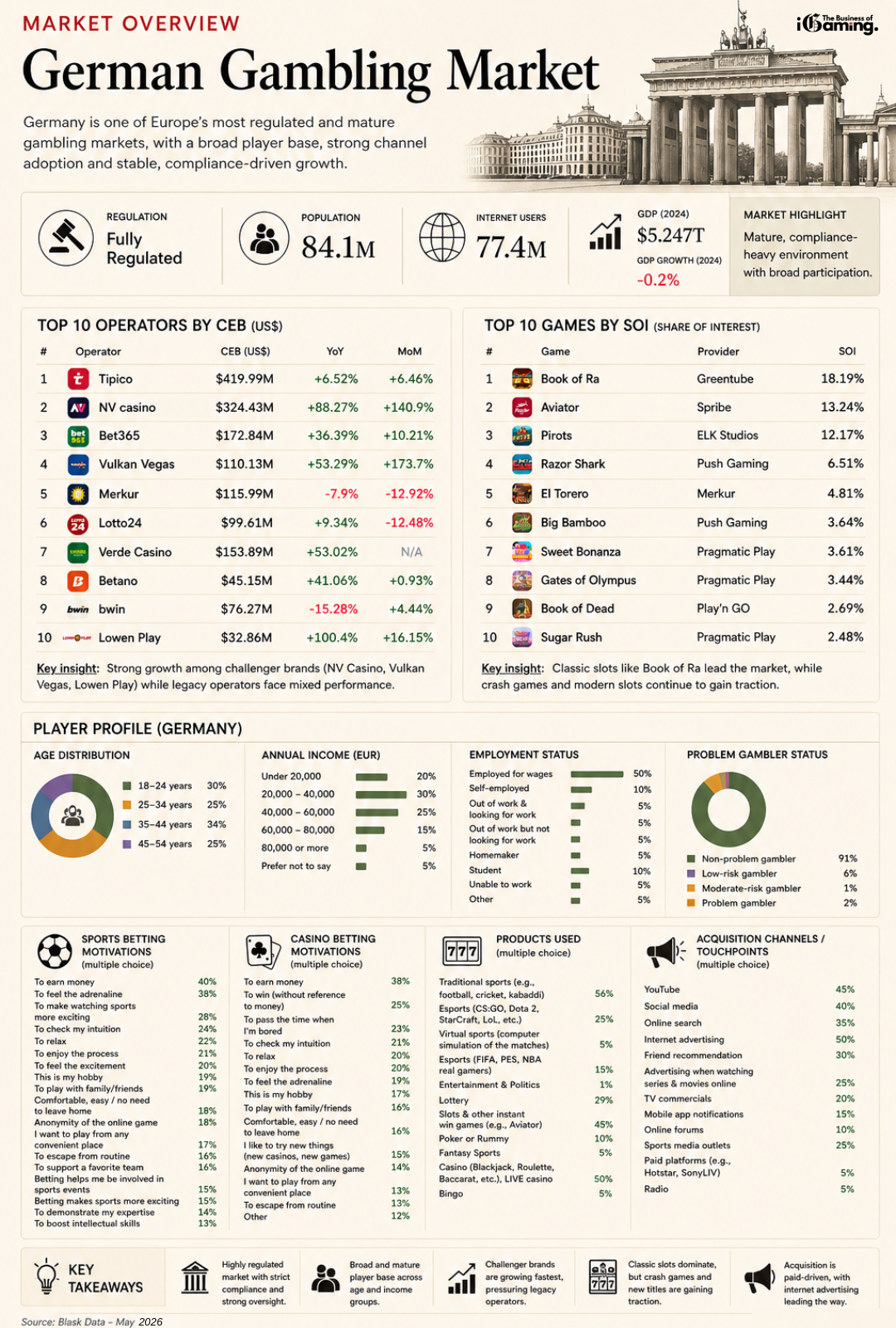

With a population of 84.1 million and over 77 million internet users, Germany offers scale. But it is the compliance-heavy framework that ultimately shapes how that scale is monetised.

A Market Built on Control, Not Chaos

Unlike emerging markets where growth is driven by regulatory shifts or sudden adoption spikes, Germany operates under a very different dynamic.

Both gambling and betting are fully regulated, and that has created a landscape where:

- Growth is steady rather than explosive

- Operators must compete within strict limits

- Long-term positioning matters more than short-term tactics

At the macro level, the environment reflects broader economic stability. GDP growth remains modest, and the market itself mirrors that — not stagnant, but measured.

This is not a market where companies “break through” overnight. It’s a market where they earn their position over time.

Operators: The Quiet Shift Beneath the Surface

At first glance, the operator landscape appears predictable. Established names still dominate the rankings, and the top positions are not unfamiliar.

But the underlying data tells a more interesting story.

| # | Operator | CEB (US$) | YoY | MoM |

|---|---|---|---|---|

| 1 | Tipico | $419.99M | +6.52% | +6.46% |

| 2 | NV Casino | $324.43M | +88.27% | +140.9% |

| 3 | Bet365 | $172.84M | +36.39% | +10.21% |

| 4 | Vulkan Vegas | $110.13M | +53.29% | +173.7% |

| 5 | Merkur | $115.99M | -7.9% | -12.92% |

| 6 | Lotto24 | $99.61M | +9.34% | -12.48% |

| 7 | Verde Casino | $153.89M | +53.02% | N/A |

| 8 | Betano | $45.15M | +41.06% | +0.93% |

| 9 | bwin | $76.27M | -15.28% | +4.44% |

| 10 | Lowen Play | $32.86M | +100.4% | +16.15% |

What stands out is not just who is leading — but who is accelerating.

Brands like NV Casino, Vulkan Vegas, and Lowen Play are growing at a pace that legacy operators are struggling to match. Meanwhile, traditional names such as Merkur and bwin are seeing declines, suggesting that brand recognition alone is no longer enough.

The takeaway is subtle but important:

Germany is no longer just a market of incumbents — it is becoming a market of execution.

Read more: The Italian Gambling Market

Games: Where Tradition Meets Modern Demand

If the operator landscape is evolving, the games segment reveals how slowly — and selectively — German players embrace change.

| # | Game | Provider | SOI |

|---|---|---|---|

| 1 | Book of Ra | Greentube | 18.19% |

| 2 | Aviator | Spribe | 13.24% |

| 3 | Pirots | ELK Studios | 12.17% |

| 4 | Razor Shark | Push Gaming | 6.51% |

| 5 | El Torero | Merkur | 4.81% |

| 6 | Big Bamboo | Push Gaming | 3.64% |

| 7 | Sweet Bonanza | Pragmatic Play | 3.61% |

| 8 | Gates of Olympus | Pragmatic Play | 3.44% |

| 9 | Book of Dead | Play’n GO | 2.69% |

| 10 | Sugar Rush | Pragmatic Play | 2.48% |

At the top sits Book of Ra, a title that has defined the German slot landscape for years. Its continued dominance says a lot about player preferences: familiarity still carries weight.

But beneath that, change is clearly underway.

Crash games like Aviator have carved out a meaningful share of interest, while studios such as Pragmatic Play and Push Gaming continue to populate the top rankings with modern, high-volatility slots.

Rather than replacing legacy titles, new formats are layering into the ecosystem, gradually reshaping player behavior without disrupting it entirely.

The German Player: Broad, Balanced, Predictable

One of the defining characteristics of the German market is the consistency of its player base.

Participation is spread relatively evenly across age groups, with strong representation from both younger and middle-aged segments. This is not a market driven by a single demographic — it is sustained by a wide, stable audience.

Income distribution also reflects a middle-heavy structure, with most players falling within the €20,000–€60,000 range. High-income players exist, but they are not the primary driver of volume.

From a risk perspective, the data reinforces Germany’s regulatory narrative:

- The vast majority of players fall into the non-problem category

- High-risk segments remain limited

- Engagement appears controlled rather than excessive

This is, in many ways, exactly what regulators intend — and it shows.

Read more: The UK Gambling Market

Why Players Play: Motivation Still Matters

Despite structural differences between sports betting and casino, player motivations reveal a shared foundation.

Sports betting leans slightly more toward adrenaline and engagement with live events, while casino play balances between entertainment and financial intent.

Across both verticals, however, two themes dominate:

- The desire to win money

- The need for accessible entertainment

That combination continues to define how products are designed and marketed in Germany.

Products and Channels: A Digital-First Reality

Germany’s product mix is still anchored in familiar formats.

Traditional sports betting remains dominant, but digital verticals — particularly slots, live casino, and emerging formats like crash games — continue to grow their share.

At the same time, acquisition has become increasingly concentrated in digital channels.

YouTube, social media, search, and paid advertising now form the backbone of user acquisition strategies. Organic growth alone is rarely enough in a market where compliance limits visibility and competition is high.

Read more: Brazil iGaming Market Analysis

Key Takeaways

- Germany remains one of the most structured and mature iGaming markets in Europe

- Growth is increasingly driven by challenger brands, not incumbents

- Classic slots still dominate, but new formats are gaining traction

- The player base is broad, stable, and regulation-aligned

- Acquisition is heavily digital and performance-driven

Final Word: A Market That Rewards Precision

Germany is not a market for shortcuts. It rewards operators who understand regulation, invest in product quality, and execute consistently over time. The days of easy growth are long gone — but for those who get it right, the opportunity is still very real.

In that sense, Germany is less about disruption — and more about refinement.

Read more: Online Gambling in the US

{kind=link}