Australia has long held a unique position in the global gambling industry.

While the country’s population of just under 27 million makes it far smaller than giants like the United States, Brazil or the United Kingdom, Australia consistently punches above its weight in gambling participation, player spend and digital engagement.

For decades, betting has been deeply embedded in Australian culture. Horse racing remains a national institution, sports betting has become mainstream entertainment, lotteries enjoy mass participation, and despite strict regulatory limitations around locally licensed online casino gaming, Australians continue to show clear appetite for digital casino products.

This combination of strong consumer demand, high disposable income, widespread internet penetration and established gambling habits makes Australia one of the most commercially attractive gambling markets in the world.

The latest market data paints the picture of a digitally mature ecosystem where sportsbook brands dominate awareness, social media has become a major acquisition channel, and casino-style gaming continues to generate significant interest despite regulatory friction.

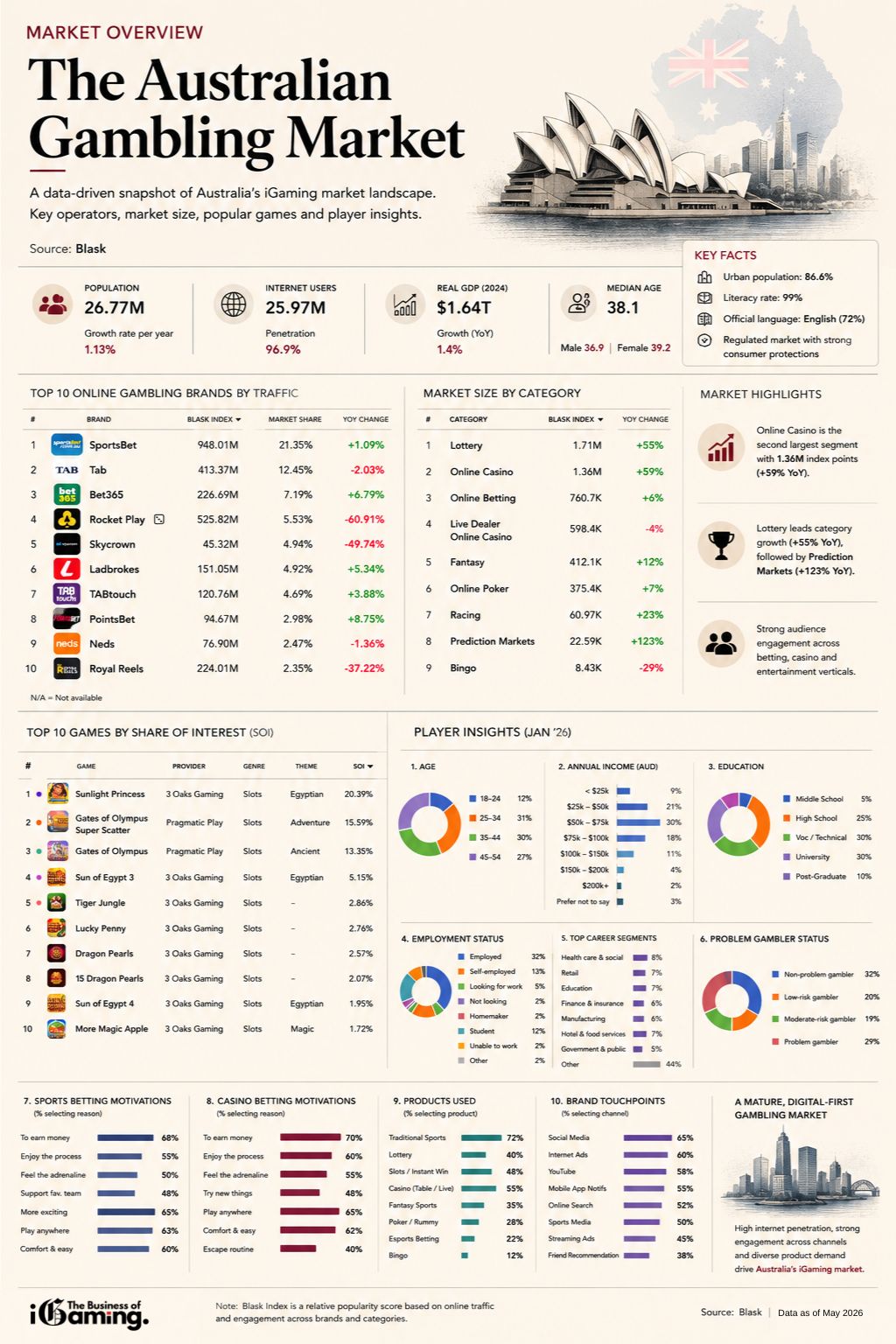

Australian Gambling Market at a Glance

| Metric | Data |

|---|---|

| Population | 26.8 million |

| Internet users | 26 million |

| Urbanisation | 86.6% |

| Literacy rate | 99% |

| GDP (2024) | $1.635 trillion |

| GDP per capita | $60,100 |

| Median age | 38.1 years |

| Annual population growth | 1.13% |

Australia combines strong economic fundamentals with one of the world’s most digitally connected populations, creating favourable conditions for both traditional gambling operators and online-first brands.

A Gambling Nation by Culture and Habit

Australia’s relationship with gambling predates the digital era by generations.

Horse racing has historically occupied a central role, with events such as the Melbourne Cup often described as “the race that stops a nation.” Sports wagering has evolved from TAB betting shops into fully digital mobile-first products, while lotteries remain deeply mainstream.

But modern Australian gambling behaviour increasingly reflects digital convenience.

Consumer data shows that 72% of players engage with traditional sports betting products, while 55% also use casino-style gaming products. Lottery participation remains significant at 40%, while newer digital entertainment formats continue to gain traction.

This creates a broad and highly diversified market where traditional betting and modern digital gambling increasingly overlap.

Read more: The Brazilian gambling market

The Operators Leading the Market

Brand competition in Australia remains fierce, particularly in sports betting.

The market is led by well-established household names that have invested heavily in product development, sponsorships and customer acquisition.

Leading operators by visibility

| Operator | Market Position |

|---|---|

| Sportsbet | Market leader |

| TAB | Legacy powerhouse |

| bet365 | Major international challenger |

| Ladbrokes | Established operator |

| PointsBet | Digital-native challenger |

Sportsbet’s dominance reflects the continued strength of sportsbook-led engagement in Australia, where sports wagering remains the largest and most visible online gambling category.

TAB continues to benefit from deep historical trust and racing heritage, while international brands like bet365 and Entain-owned Ladbrokes remain highly competitive.

PointsBet represents the newer generation of mobile-first sportsbook operators focused on product innovation and aggressive digital acquisition.

Read more: The Italian Gambling market

Online Casino Demand Exists Despite Regulatory Constraints

Australia presents an unusual contradiction. Locally regulated interactive casino gaming remains heavily restricted under the Interactive Gambling Act framework, yet player demand for casino-style experiences clearly exists.

Consumer product usage data shows:

- Casino products: 55%

- Slots / instant win games: 48%

- Poker / rummy: 28%

- Bingo: 12%

This suggests that while regulation limits domestic operator participation, consumer appetite has not disappeared.

Instead, demand has shifted toward offshore brands, alternative gaming formats and international digital operators.

For affiliates, suppliers and technology providers, this makes Australia strategically interesting despite legal complexity.

Fastest Growing Gambling Categories

The market is not static. Several verticals are showing notable momentum.

High-growth categories

| Category | YoY Growth |

|---|---|

| Prediction Markets | +123% |

| Online Casino | +59% |

| Lottery | +55% |

| Sports Betting | Strong / mature |

Prediction markets remain a smaller niche, but their rapid expansion reflects broader consumer appetite for event-based speculation.

Online casino growth is particularly noteworthy given Australia’s regulatory environment, reinforcing the idea that consumer demand continues to outpace legal supply structures.

Lottery’s resilience also highlights how traditional products remain relevant even in increasingly digital ecosystems.

Read more: Online Gambling in the US

Who Is the Australian Gambling Consumer?

The demographic profile reflects a relatively mature, economically stable audience.

Age profile

| Age Group | Share |

|---|---|

| 18–24 | 12% |

| 25–34 | 31% |

| 35–44 | 30% |

| 45–54 | 27% |

The market is overwhelmingly adult working-age consumers rather than youth-led experimentation. Income data also suggests meaningful spending capacity.

Income profile (AUD)

| Income Band | Share |

|---|---|

| Under 25,000 | 9% |

| 25,000–50,000 | 21% |

| 50,000–75,000 | 30% |

| 75,000–100,000 | 18% |

This aligns with Australia’s relatively high GDP per capita and strong consumer spending environment.

Why Australians Gamble

Motivation matters because it shapes retention, acquisition and product design. For sports bettors, the strongest motivations include:

- To earn money (68%)

- Betting makes sport more exciting (65%)

- Convenience of playing from anywhere (63%)

- Easy home access (60%)

- Enjoyment of the process (55%)

Casino players show similar behavioural drivers:

- To earn money (70%)

- Play from anywhere (65%)

- Convenience (62%)

- Enjoy the process (60%)

- Adrenaline (55%)

This reinforces an important commercial point: Australian gambling behaviour is not driven purely by financial incentive. Entertainment, convenience and emotional engagement play equally important roles.

Read more: The Swedish gambling market

Marketing Channels That Matter

Customer acquisition in Australia is increasingly digital-first.

Key discovery channels

| Channel | Reach |

|---|---|

| Social media | 65% |

| Display advertising | 60% |

| YouTube | 58% |

| Mobile app notifications | 55% |

| Online search | 52% |

| Sports media | 50% |

Social media’s dominance highlights changing acquisition dynamics. Traditional television remains relevant, but digital performance marketing, app engagement and creator-led discovery are clearly reshaping the landscape.

For affiliates, this is a crucial takeaway. Search still matters, but it no longer operates alone.

Game Providers Winning Player Attention

Provider visibility shows clear concentration. Pragmatic Play remains a dominant global force, while 3 Oaks Gaming appears to be performing particularly well in player interest rankings within this dataset.

Popular titles include:

- Sunlight Princess

- Sun of Egypt

- Tiger Jungle

- Gates of Olympus variants

This reflects broader global patterns where mythological themes, volatile mechanics and mobile-first slot design continue to perform strongly.

Read more: The Netherlands iGaming Market

A Responsible Gambling Reality Check

Australia’s gambling opportunity also comes with social challenges. Consumer segmentation in the dataset shows:

| Status | Share |

|---|---|

| Non-problem gambler | 32% |

| Low-risk gambler | 20% |

| Moderate-risk gambler | 19% |

| Problem gambler | 29% |

Even allowing for methodology caveats, this is a reminder that gambling growth and player protection remain inseparable discussions.

Responsible gambling frameworks, advertising controls and affordability discussions will remain central to Australia’s long-term market evolution.

Why Australia Still Matters

Australia may not be the largest gambling market by population. But in terms of monetisation potential, digital maturity and player engagement, it remains one of the most strategically important markets globally.

It combines:

- strong legacy gambling culture

- affluent digital consumers

- sportsbook scale

- persistent casino demand

- competitive operator dynamics

- sophisticated acquisition channels

For operators, suppliers, affiliates and investors, Australia remains a market worth watching closely.

Read more: France iGaming market

{kind=link}